Select a region

Jersey’s Treasury Minister has published a plan which would see the island taking on debt to the tune of more than £1.8 billion, not including interest. That would mean that the island's ratio of debt to the total value of the economy, would leap to 39%.

That number includes £756 million for the new hospital, but also a further £450 million to re-finance liabilities in the public sector employees, and teachers, pension schemes.

The figures have been released in a ‘debt framework’, published by Treasury Minister, Deputy Susie Pinel. The figure of £1.8 billion does not include interest, and is made up of:

The report paints a new landscape for Government finances in an Island which has long prided itself on low levels of borrowing: last year, debt as a proportion of the total value of the Jersey economy was just 5.4%.

This year, it is due to jump to 34.2% because of borrowing for covid and the new hospital.

If the debt strategy is backed by the States Assembly, the ratio will increase to 38.6% by 2024.

The report recommends that Jersey should set this ratio, of ‘debt-to-gross domestic product’, at between 30% and 40% in the medium term, which it says should not affect the island’s credit rating, which in turn influences how much it can borrow.

Pictured: The Government plan to borrow £756m to fund the new hospital at Overdale, to be paid back within 40 years.

However, the report does indicate that the island’s current “AA-” credit rating from Standard and Poor’s could fall, potentially due to factors outside of Jersey’s control, such as the UK’s rating and prevailing market conditions, as well as the state of the local economy.

It says: “Jersey will aim to maintain an investment grade rating (BBB- and above) under all market conditions. This will support the ability of the Government to issue debt or to access short-term facilities if warranted by the prevailing environment.”

Pictured: Jersey's Debt to GDP ratio until 2024

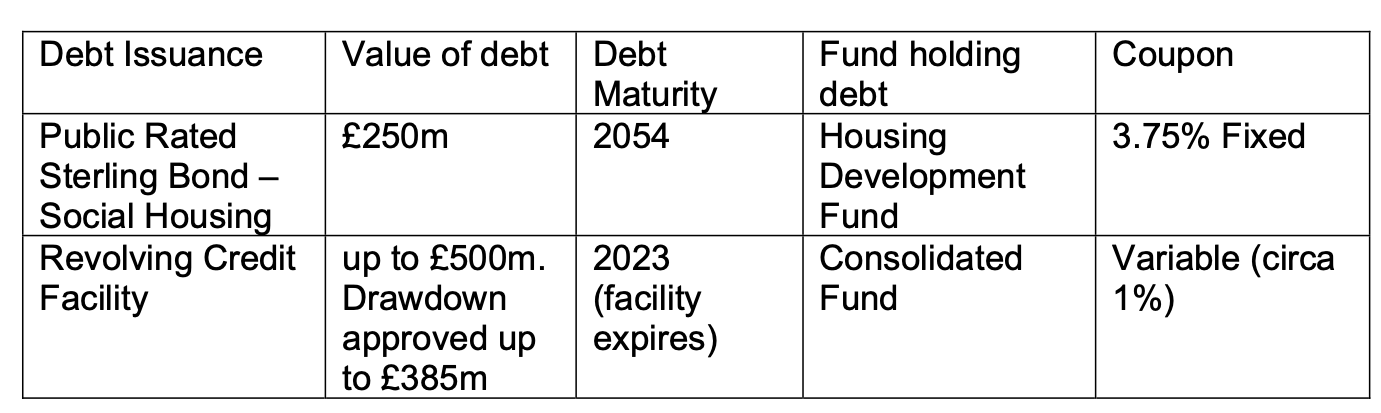

Some of the debt referred to in the framework has already been agreed and taken out, such as a £250m bond in 2014 to fund improvements in social housing, and the up-to £500m ‘revolving credit facility’ to pay for the Government’s pandemic response.

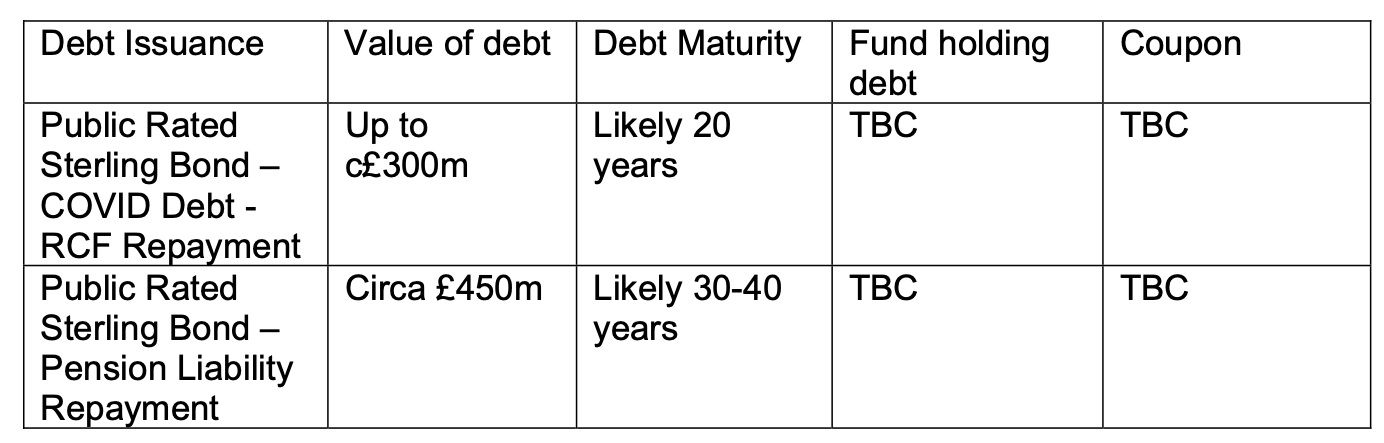

However, new debt is proposed:

Pictured: debt which has already been agreed.

Pictured: debt which is proposed and awaiting approval later this year.

Pictured: future debt which Ministers believe the island will need.

The report says: "The Council of Ministers recognises that financing may provide a valuable source of funding to assist the public administration in meeting its objectives. When considering financing, Council will ensure that all funding alternatives are fully considered.

For the purposes of this policy, financing is considered to be: loans from external institution; the issuance of bonds; finance leases (not operating leases); assignment of debt from a third party; and sale and leaseback transactions.

"The debt policy applies to debt put forward for approval by the States Assembly. It is not designed to limit the Minister’s ability to operate transitional debt arrangements, such as bank overdraft facilities and smaller short-term debt arrangements, [as outlined in the public finances law].

"These transitional debt arrangements are designed to allow for the efficient management of the liquidity requirements of the States and not as a long-term funding solution."

Comments

Comments on this story express the views of the commentator only, not Bailiwick Publishing. We are unable to guarantee the accuracy of any of those comments.