Guernsey’s 2024 States Accounts are the first to be fully compliant with International Public Sector Accounting Standards.

That means they give a ‘true and fair’ view of the island’s actual financial position – the implication being that past accounts didn’t do that.

Being IPSAS compliant means Guernsey’s accounts can now be compared to other jurisdictions that also meet the required standard – something that wasn’t previously possible.

Deputy Jonathan Le Tocq said it’s something that has been on the agenda for a long time.

“It has been something that many accountants and critics of the States of Guernsey have asked for. Certainly, 10 years ago when I was Chief Minister there were calls for that, and it’s taken a long time to do that,” he said.

“Prior to that, we had accounts that were done, if people are familiar, in more of a sort of management account. It didn’t take into account, for example, fixed assets so buildings and machinery, equipment and all those sorts of things that the States obviously owns a large amount of, and neither did it take into account the liabilities, although it did some but not others. It was a bit of a mix, and therefore this is the first time that our independent auditors Grant Thornton have been able to say, this is a true and fair assessment.

“We’ve not had that in the past, but that is important for us. There’s a lot more detail, so if we’re going to make evidence, evidence based decisions, then this is the first year that we can look at everything in proper context.”

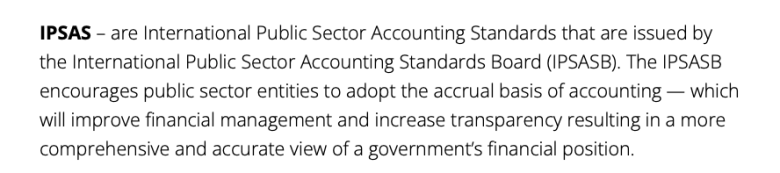

IPSAS

International Public Sector Accounting Standards are a set of accounting standards issued for use by public sector entities worldwide when preparing their financial statements.

IPSAS are based on the International Financial Reporting Standards (IFRS) but are tailored for the unique characteristics of public sector entities.

A quick google gives numerous examples of other places where IPSAS is held up as a high standard for accounting within the public sector.

The States says Guernsey is one of only 17 jurisdictions that now fully adheres to IPSAS.

It says “this gives independence and impartiality to the accounts and their presentation”.

It has taken a long time to get to this point though with the work described as a “significant undertaking over several years”.

In 2024, Deputy Heidi Soulsby – as Vice President of P&R – said changing the way Guernsey’s accounts were presented would bring many benefits in the long term.

“It’s not about accuracy,” said Deputy Soulsby.

“It’s about the presentation and following standards. The concept of accuracy is an interesting word in the world of accountancy. (The accounts) have been audited for many years. So from an accuracy point of view, I don’t think the public should be concerned.

“The issue is about using standards that are understood and they can be referred to and compared to other places. So that’s the nub of it, really. And on top of that, it’s not just IPSAS – we’ve added more disclosures that we haven’t had to in the past, and I think that again it gives more information for users of the accounts, in this case the public, the taxpayer to see where their money is going.”

-£44m

Guernsey’s £44m deficit is the ‘Core’ financial position of the States.

This reflects the ‘day to day’ running costs of the island.

It reflects all the money paid in – through our taxes, social security, and other revenue raising payments – and all the money paid out in providing our ‘core services’ such as running the hospital, schools, and public services.

In publishing the accounts with the headline shouting a £44m deficit, P&R said it believed “the focus should be on the financial position of the States of Guernsey ‘Core’,” not on assets that it can’t access such as profits or losses made by the trading entities.

The £44m deficit is therefore made up of income from general revenue minus the cost of running the island’s public services.

The £44m deficit reflects a £9m deficit in general revenue, a £13m deficit in social security income/outgoings, and a £22m deficit caused by the island’s non-infrastructure expenditure – which includes things like the IT transformation project, elements of the revenue service programme, and the introduction of the electronic patient records system.

What’s included

Being IPSAS compliant means that the States’ accounts now include all of its trading entities.

Previous accounts didn’t include things like Guernsey Electricity, Guernsey Water, Guernsey Ports, Guernsey Waste, or Guernsey Post.

Companies owned by the States to manage other entities like Aurigny and the oil tankers- through Cabernet and James Co, are also now included.

Previously they weren’t because they represented services that were outside the day to day control of the States with limited impact on the island’s operating income and outgoings.

The Group Accounts compiled under IPSAS means that all States owned bodies must be included.

However, the headline figure of a £44million deficit does not include them.

When the commercial entities respective surplus or deficits are brought into the financial picture it gives a different picture of island finances – but P&R says that wouldn’t be a fair reflection of the true situation.

When included – and published as the ‘Group accounts’ – rather than the ‘Core accounts’ – the deficit is reduced to £18.8m.

That figure varies even more wildly when the island’s investments are included.

States investments

States of Guernsey Investments were valued £130m higher at the end of 2024 than 2023 but as an investment valuation – as opposed to an investment return – meaning they’re not included in the core accounts either.

The public purse did not receive £130m from those investments and nor will it as they haven’t been divested and won’t be any time soon either.

Deputy Le Tocq said they remain invested as part of the States portfolio and as with any investments valuations regularly fluctuate.

“If anybody has any savings or investments, they know that if you keep on looking at them, you will see they go up sometimes, and they go down sometimes. Also, these are often funds that are allocated at some time in the future to something and so if we get rid of them, or if we use them for something, we need to replenish them in some way.

“It’s useful to know what their value is, but it is a snapshot of the 31st of December 2024 and they’re not realised increases, even though they’re substantial.

“To a certain degree, they’ve helped us look at the overall picture and say we’re not in crisis, and I would agree with that, but we can’t rely on them.

“If we started spending out of our reserves without replenishing those reserves, then we’re just putting a problem into the next generation, and that is something that will be very foolish for us to do.”

If the accounts are looked at with the investment valuation included the deficit changes into a surplus – at £20m for 2024.

As that money can’t be spent on anything else because the investments haven’t been divested it’s best to pretend it doesn’t exist and stick with the core accounts instead.

The future

The current P&R has headlined the £44m deficit figure – but in reality the States accounts show a £56m deficit.

That is what P&R says is the number when we look at the “structural, annual deficit”.

Retiring P&R Vice-President Deputy Soulsby said: “we’re not raising enough through taxes to fund the services our community relies on. It is clear that this will need the collective attention of the incoming assembly”.

That incoming Assembly is due to be sworn in on 1 July, with the new P&R President elected that same day before the P&R members are appointed on the 2 July.

The new States – once everyone has been elected to committees or left on the back benches – will debate the Accounts on 15 July.

The looming prospect of the introduction of GST+ is expected to come back before the States early in this term, but after debating the accounts and holding their first scheduled meeting in July, the States will then break until September, with the 2026 budget scheduled for debate in November.