Select a region

Supply chain challenges are just one of the reasons that cost of living is rising so quickly at the moment. But they are also causing problems for manufacturers who are struggling to acquire vital components.

Recent figures released for the UK car industry show a slowing down in activity, with new car sales in May down 21% on last year[1]. This is partly because consumers are reining in their spending, but also because there is a shortage of one vital component that goes into every modern car: microchips. In this brief article Ryan Harrison, Head of Canaccord Genuity Wealth Management in Jersey, explains the root cause of the problem.

The invention of the semiconductor chip is right up there with humanity’s greatest achievements. These tiny items, made of silicon, cobalt, and copper, are central to all modern technology and sit inside almost every electronic device, including your car, phone and computer.

Recently, the problem has been not having enough of them. Last year many car manufacturers, including GM and Ford, either shut down or slowed down production because they couldn’t get enough chips. For example, Ford’s F-150, the best-selling truck in America, was held hostage to a semiconductor with a price of just US$0.25.

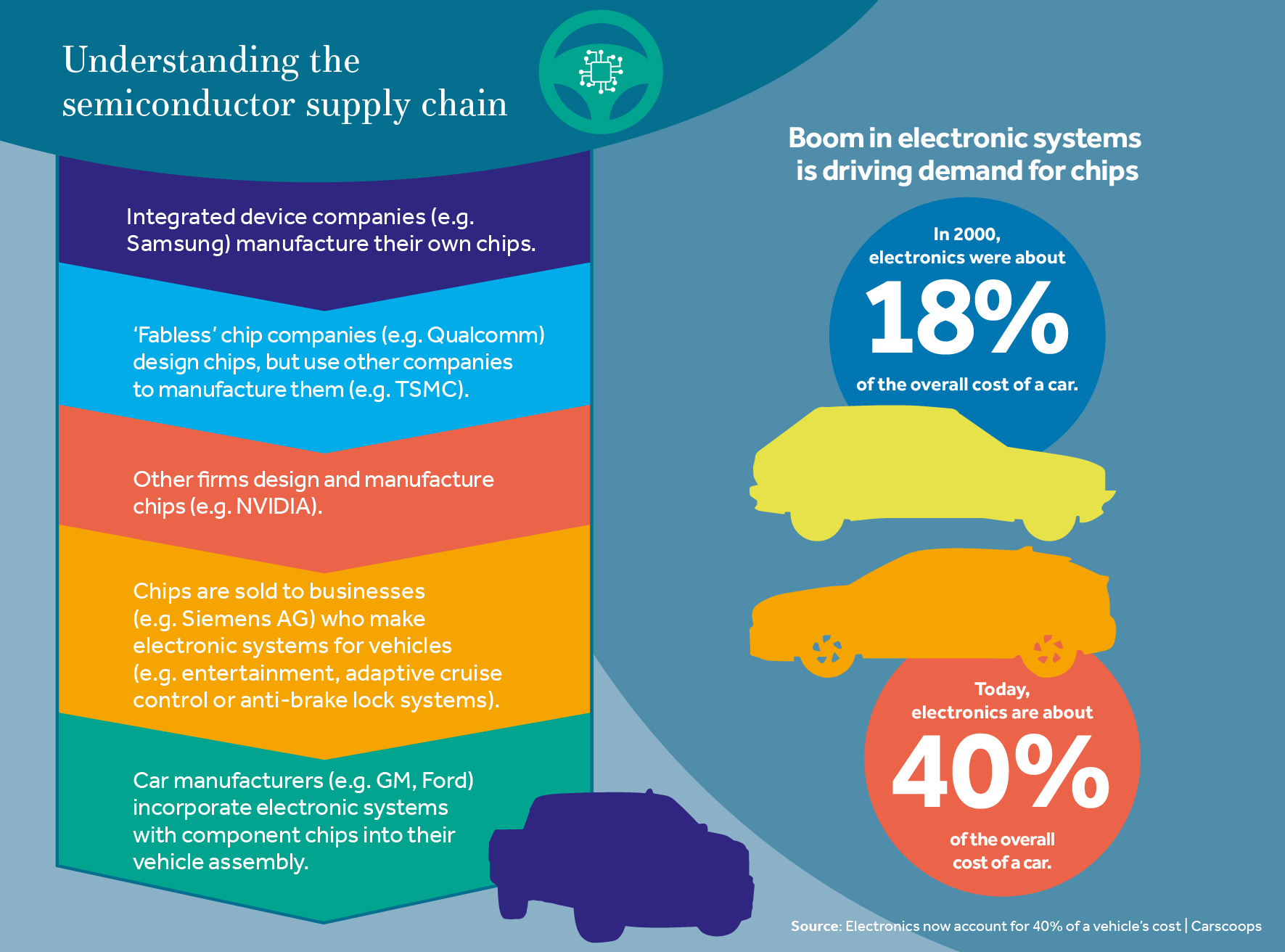

What is causing the current chip shortage?

Let’s start with the demand side.

The percentage of a car made up of electronics has been steadily increasing, to about 40% of the total cost of a car today. In 2000, it was around 18%. This seems obvious when you think of safety features like adaptive cruise control, or automated stopping if there’s a pedestrian in front of you.

Secondly, when COVID-19 hit, many car manufacturers assumed car demand was going to fall sharply. So they cut back orders. At the same time demand went through the roof for consumer electronics such as laptops, due to the rise in working from home. When it later emerged that car sales weren’t going to be as dramatically impacted by COVID-19 as initially thought, the manufacturers went back to the suppliers, and discovered the chips were not available.

Unfortunately, it takes dozens of weeks to make a new semiconductor, and you can’t turn production off and on quickly. When orders get cancelled, lines are retooled to build other chips. To restore the production line for your chip could take a year.

The biggest customers for chips are mobile phone makers. If Apple places an order, that’s billions of components, and it's a reliable customer, so would be prioritised ahead of automotive companies. Car chips can also be harder to make. Their temperature range, operating lifetime, and failure rates have to be better. While your laptop’s light sensor can go bad without endangering lives, your car’s adaptive cruise control can't.

Some of the chips that cars need are also essentially the same chips that are used in smartphones, bringing car manufacturers directly into competition with phone companies for the already limited supply.

Fighting over a fixed supply

The world has a fixed semiconductor manufacturing capability, but infinite demand. Semiconductor factories are incredibly expensive (say US$10bn) and relatively low margin to build, and might be obsolete in five years. So they depreciate quickly, contributing to chip supply problems.

In turn, the investment industry has rewarded companies that design chips, but don’t actually make them, as they provide higher profit margins. Companies that both design and manufacture, have also performed extremely well in terms of investment growth compared with the global market as a whole.

Taiwan, one of the world’s biggest manufacturers of semiconductors also recently went through a drought, exacerbating the shortage because the process of chip production is highly water-intensive.

East is east, west is west

If there were no politics, China would be the obvious choice for manufacturing semiconductors.

However, companies in the semiconductor tool chain in the United States have to apply for licences to sell to Chinese companies. The US is worried that China will buy semiconductor manufacturing equipment, reverse engineer it, infringe on the intellectual property, and then make their own semiconductors. China’s explicit goal is to have the number one semiconductor design and manufacturing industry in the world by 2030.

Can China get there? They don’t want to stop at just chips. They want the entire technology supply chain. In the next 10 years, will there be a Chinese operating system running on a Chinese chip, designed by China? If so, we will really have two competing world ecosystems.

What are the implications for investors?

The implications for investors can be seen in two ways. Firstly, a technology supply chain affects plenty of businesses outside the technology sector. Secondly, this presents opportunities to invest in companies that can innovate to make this process more efficient or resilient. As ever, whenever there is a problem, creative companies will find a solution.

Investment involves risk. The value of investments and the income from them can go down as well as up and you may not get back the amount originally invested. Past performance is not a reliable indicator of future performance.

The information provided is not to be treated as specific advice. It has no regard for the specific investment objectives, financial situation or needs of any specific person or entity.

This is not a recommendation to invest or disinvest in any of the companies, themes or sectors mentioned. They are included for illustrative purposes only.

The information contained herein is based on materials and sources deemed to be reliable; however, Canaccord Genuity Wealth Management makes no representation or warranty, either express or implied, to the accuracy, completeness or reliability of this information. Canaccord is not liable for the content and accuracy of the opinions and information provided by external contributors. All stated opinions and estimates in this article are subject to change without notice and Canaccord Genuity Wealth Management is under no obligation to update the information.